The takeaway?

Investing based on emotion rarely ends well. No one has a crystal ball, but one thing is certain: letting emotions dictate your strategy is a fast track to underperformance. Now, let’s talk about the bright side…. Despite the carnage in equities—with most major indexes down 10–20% and individual stocks hit even harder—diversification is finally doing its job again. Bonds have held up well amid falling interest rates. The U.S. Aggregate Bond Index is actually up 2–3% year-to-date. In addition, various types of equities have posted vastly different returns during the decline. Growth is down a lot more than value, small is down more than large. Just like last time(s), valuations were stretched. Stocks were a bit pricey. Old stogy bonds were a decent add with 4 to 5 percent yields. Lots of folks (not our clients, but others) were chasing returns by adding to the things that were working in the immediate. The “magnificent 7” were todays variation of the nifty fifty and the internet plays. As with most of these things, the balanced/diversified and conservative crew is down some. The more risky are down more. The Nuevo aggressive are getting walloped. You get what you pay for.

Enough philosophy, down to the inner workings. Where were we going in and what’s the forward. Quite simply, we manage portfolios on what’s called a “tactical allocation basis”. They are not static, but change over time with expectations and economics factored in. Think in terms of a stop light, green-yellow-red. Red for underweight equity, yellow for caution (neutral), Green for overweight equity (more optimistic). We state our position when we put out a ranting and even give some words as to specifics. In this case we were neutral with low/intermediate duration on investment grade fixed income.

Looking ahead, being neutral gives us a lot of wiggle room. If this current event grinds lower, and valuations get better, you can expect us to be buyers. Rebalance plus add some to equity. We haven’t been “green” since mid 2022 but more downside might get us there in the near term. And, as always, we use downside volatility to tax loss harvest and this time will be no different.

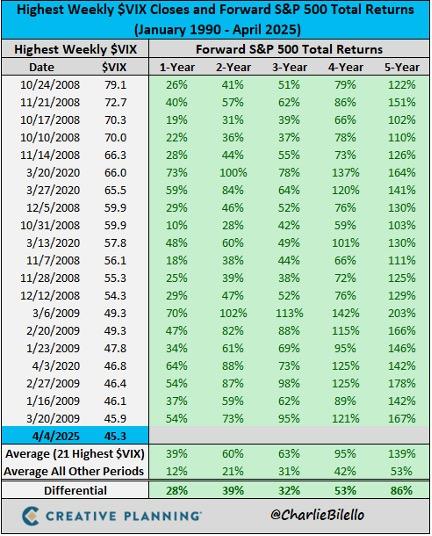

We will leave you with one final note: last week’s VIX reading ranked among the top 20 highest since 1990. The VIX measures market volatility—how “nervous” investors are. You don’t need to understand the mechanics, just this: historically, when volatility has spiked to this level and held for a full week, forward returns have been some of the strongest on record. Makes sense when you think big picture.

|