In our view, and as we wrote about before, this was a possible/eventual outcome due to all the free money and monetary actions of 2020. Rampant inflation, a broken labor market, and a fragile supply chain left the Fed with little choice but to tighten financial conditions. Pumping the brakes before the car hit the wall was the only reasonable option. The pure implication of steep short-term interest rates increasing has sent shockwaves throughout the bond and equity markets.

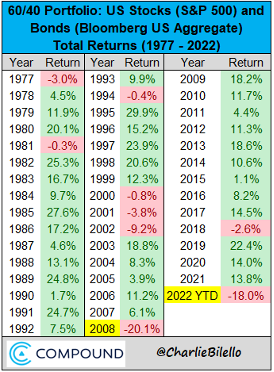

Looking at the chart below, you’ll see that as of June 21st, a 60/40 portfolio comprised of 60% S&P 500 (equity) and 40% US AGG (Bond) would be down 18% on the year. This is the balanced portfolio’s second-worst start to a calendar year since 2008. While this was not good, keep in mind, that investors who ditched their plan of diversification did worse. Much worse.

There is no sugar coating this economy or these returns. Not good is an understatement and the damage to equity markets and the real economy is significant. The good news… we’ve been here before. This will be the 20th recession in US history and the 12th since 1948, which comes out to about 1 recession every 6 years since the late 40s.

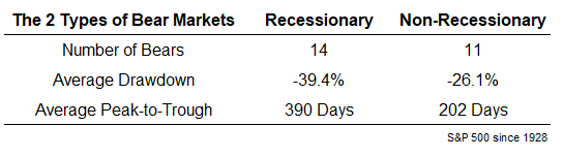

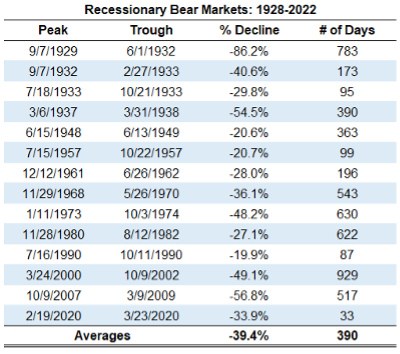

As for bear markets, this is our 26th bear market since 1928. As you’ll see below, this bear market will be the 15th bear that occurs during a recession. The average drawdown throughout those bear markets is nearly 40%.

If we dig into the details a little further, you’ll notice that a few of the bear markets since 1928 play a large role in generating the average drawdown number. If you were to just remove the three major drawdowns during the Great Depression and the 2008 global financial crisis, the average drawdown would be around 30%. And if you look at where we are today, there are several sectors of the market that are down over that 30% mark.

This by no means is a proclamation that we are at the bottom. It’s a historical reference. However, when you look at the current environment it doesn’t appear that we are headed towards a great depression or global financial crisis. It was necessary for the federal reserve to eventually normalize rates, and unfortunately, investors are feeling the brunt of it. Doing so in the manner it was done should have some mitigating effect on depth and duration.

From here, we remain slightly overweight equity in our models and short to intermediate on the yield curve. Yes, we believe the headlines will get worse and the media-induced frenzy is not over, but we feel a lot of the damage is done. Markets are predictive (leading) indicators, and they move first. We are looking ahead to the eventual end of this one and the formation of the next economic up cycle. We will continue to keep our eye on the inflation data and yield curve in the coming months.

As always, please don’t hesitate to reach out if you have any questions.

Frank

Ed

Tammy

Retirement Capital Advisors

800 Battery Ave SE

The Battery, Suite 100

Atlanta, GA 30339

Securities and Advisory Services offered through Commonwealth Financial Network®, member FINRA/ SIPC, a Registered Investment Adviser.

This writing is for the clients and associates of Retirement Capital Advisors only. It is not intended as specific investment advice. You should talk to your own financial advisor about specific investments. No guarantees are implied or given and investing involves risk of loss of money. All statements made herein are forward-looking and assumptive and do not guarantee any outcome.

All indices are unmanaged, and investors cannot actually invest directly into an index. Unlike investments, indices do not incur management fees, charges, or expenses. Past performance does not guarantee future results.