Coming into 2022, the economy and equity markets were on quite a tear… On the back of high corporate earnings, low unemployment, historically low interest rates, almost no inflation, and unprecedented government intervention throughout the pandemic, we saw the S&P 500 return roughly 31% in 2019, 18% in 2020, and 28% in 2021 in consecutive years.

This economic environment also led to things such as: strong consumer balance sheets, home equity at an all-time high, and a demand for goods and services that we haven’t seen in quite some time. This continued along for the better part of two years, until late 2021, when inflation reared its ugly head. This is where most of the positive headlines ended… Low interest rates, government subsidies, a broken supply chain, a war in Ukraine, soaring energy prices, among many other things, led to inflation reaching 9.1% in June 2022, which was nearly a 50 year high.

To combat this rampant inflation, the federal reserve tightened short-term interest rates at a record clip. In 9 short months the fed funds target went from 0 to over 4%. This was the most aggressive Fed tightening cycle in history. Additionally, the Fed embarked on Quantitative tightening of the money supply which added to the actions. As a result, investors struggled.

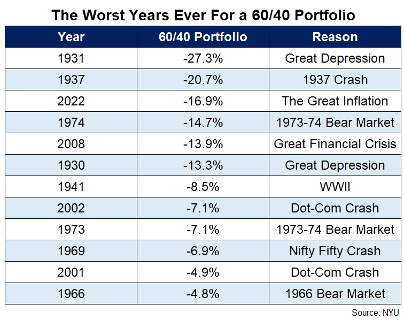

2022 was the 7th worst calendar year for the S&P 500 (-18.1%). The worst year in history for the US Aggregate Bond Index (-13%). The 3rd worst calendar year for a 60/40 portfolio (-16.9).

The pain is real, and we don’t want to shy away from it. Just like the 2022 tightening cycle, these returns are unprecedented. Typically, when equities sell-off, you have bonds in your portfolio to soften the blow. However, this time around, unless you were in 100% cash or 1–3-month T-Bills, you couldn’t escape the damage.

Looking ahead and going forward- it’s important to acknowledge what has happened but remain focused on the bigger long-term picture. Could stocks and bonds go down more? Sure. But if we use history as a teacher, all things cycle. The risk of loss, which we are all unfortunately experiencing at the moment is why investors have earned an annual return of 4-6% in bonds and 8-10% in equites. Volatility is inherent to investing. 70% of calendar years the stock market is higher, and 65% of the time the market is positive following a negative year.

As long-term, plan driven investors, it is hard not to get excited about equity valuations and global bond yields going forward. Again….. going forward.

Positioning (or where we are now)

Headed into to 2023 we are slightly overweight U.S equity, underweight international stocks, with a lean towards short duration bonds and cash. While nobody can predict specific market inflection points, the longer-term outlook is pretty good. If markets re-test October 2022’s lows, we will look to put some of the dry powder to work. Keep in mind the investor sentiment and psychology are bad now which usually means we are closer to the end of the Bear vs the beginning. Just an observation.

Retirement Capital Advisors looks forward to continuing our relationship with you in 2023! As always, don’t hesitate to reach out for any reason. We are also pleased to announce that we have the capacity to take on new clients in the new year so feel free to refer your friends and family. Our team is here for you.

Frank Vance

Retirement Capital Advisors

800 Battery Ave SE

The Battery, Suite 100

Atlanta, GA 30339

Office- 412-722-3795

Securities and Advisory Services offered through Commonwealth Financial Network®, member FINRA/ SIPC, a Registered Investment Adviser. Fixed insurance products and services are separate from and not offered through Commonwealth Financial Network

Disclaimer: The term markets, market, S&P 500, or any other reference to financial markets are notional concepts and not specific investment advice or suggestion. This article does not constitute specific investment advice, and none is implied or inferred. This article is for clients of Retirement Capital Advisors only. Investing entails risk of loss of principal and no guarantee of returns are inferred or implied